")

International Customer Controlling – A look beyond borders

Amid all the Big Data, have we lost sight of our customers? Big Data poses special challenges. Despite or perhaps even because of Big Data, many of us are still „flying blind.“ Yet the BI tools that make Big Data manageable and meaningful to use are exactly what enable us to take a further important step in customer controlling.

We are international – our customers are too! Not every customer is tied to a branch or a country. A bad customer in one country does not necessarily mean a bad customer for the group. Business processes are internationally connected. For example, it is no longer a rarity that a global key account manager (GKAM) may work for corporate headquarters in the US and yet close a big order for Mexico. So, where do you show the costs of this GKAM now – on the income statement of the US, at corporate headquarters, or in Mexico, where the revenue from the order is actually recorded?

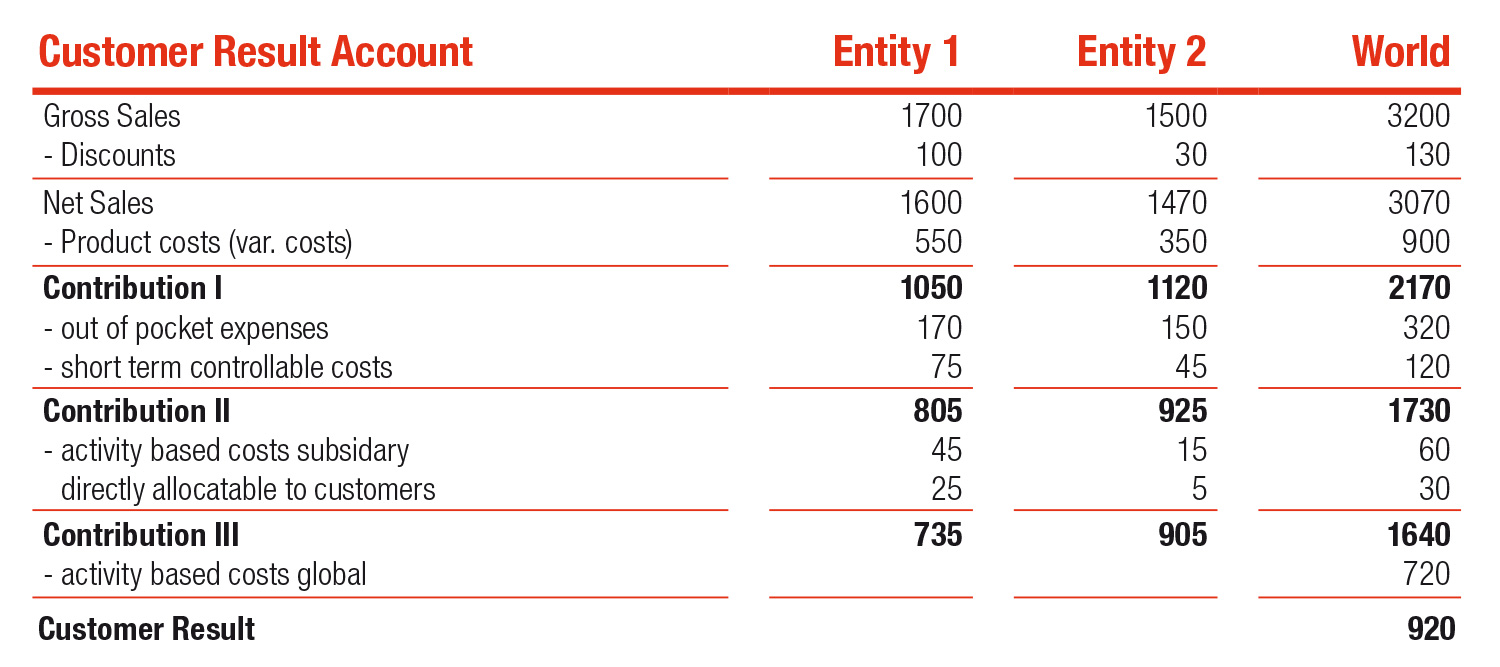

An international customer result account provides transparency. To do that, you need worldwide multi-level contribution accounting by customer. Initially, we compile the product margins on the customer orders. Then I recommend that you deduct cash-effective costs that are controllable in the short term. Depending on the sector, these can be, for example, sales reductions in the broader sense, service charges at the retail level, warranty and goodwill costs, catalogue participations, entertainment, etc. After a contribution margin II is calculated, we deduct the expenses associated with „looking after“ the customer. These include, for instance, activity-based expenses for order processing, consulting and training services as well as the costs for complaint management and customer support by our internal and external sales teams or the global key account team.

Don’t worry about some gaps! When segmenting customers, it doesn’t matter whether the customer result is exactly right. Rather, what’s important is the order of magnitude and the relative position in comparison with other customers. After all, it is certainly true that a customer who places daily orders causes more ordering expense than one who places an order just once a week, meaning it doesn’t matter if you book costs of 9 or 11 for an individual order.

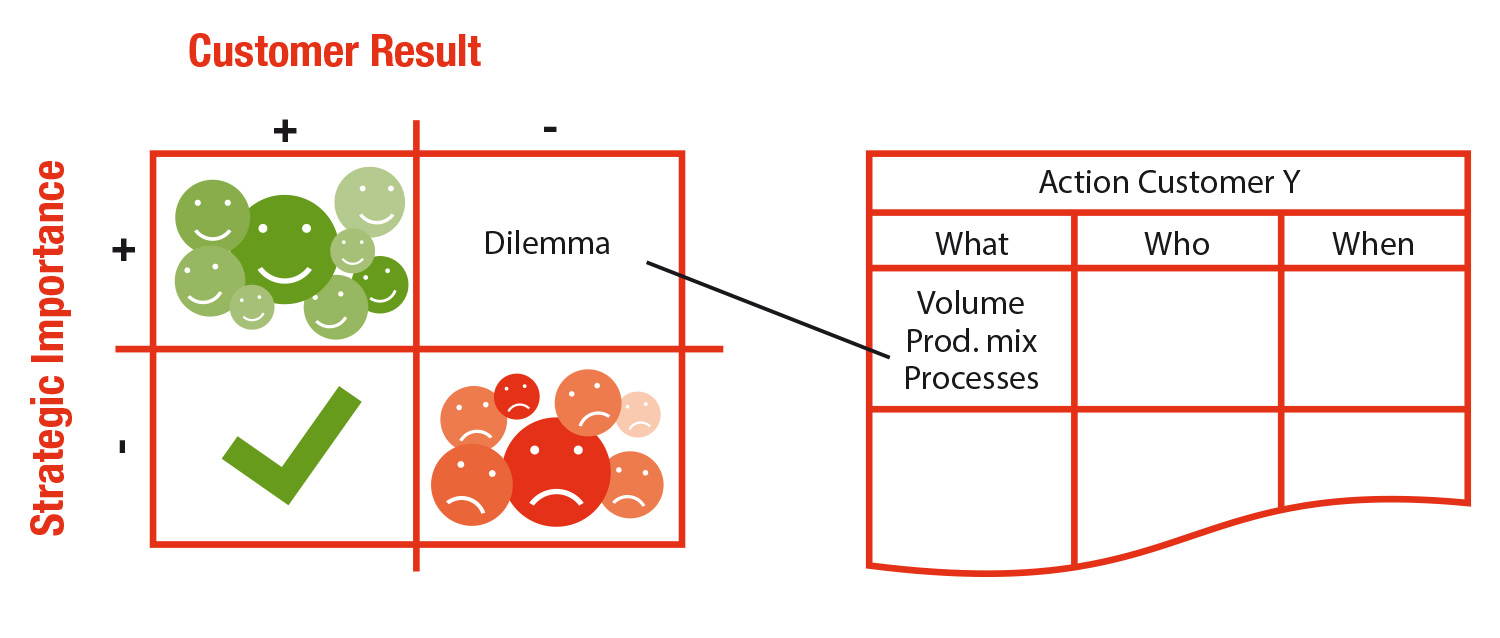

Customer portfolios allow a holistic view. In addition to the operating customer result, the strategic importance of the customer must be taken into account, too.

Who are your „dilemma customers“ – i.e., those with high strategic importance but a poor customer result? How many of them can we afford (budget!), or is there something we can do about the activity-based expenses associated with these customers?

To achieve sustained success in customer relationships we need a holistic view of our customers.

Happy customer controlling

Dietmar Pascher

Published in Controller Magazin Spezial, 2014, page 6